Silicon Valley Bank has just published its 2026 Direct-to-Consumer Wine Report, built on 450 family wineries and their 2025 trading. It's the closest thing the wine world has to a mirror.

It is US data, and the temptation is to wave it away on that basis. I would not - the patterns in it travel far better than you would expect.

If I had to reduce the whole thing to a single line, it is this: the gap between the wineries that are growing and the ones that are struggling now has very little to do with their size, their region or their luck. It is about how they behave.

The headline: a widening split

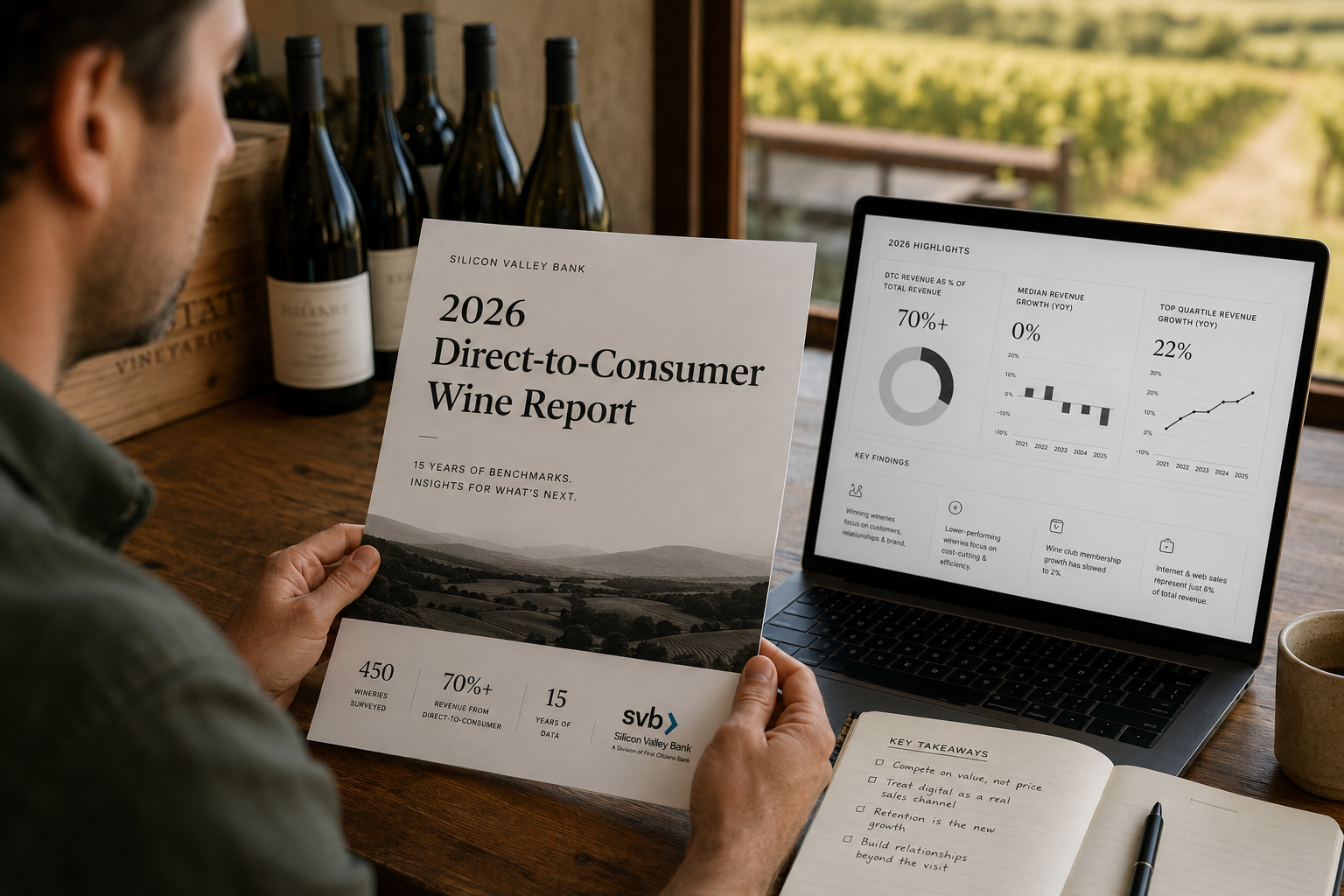

In 2025, the top quartile of wineries grew revenue by 22%. The bottom quartile fell by 13%. The median winery had no growth at all. Same market, same headwinds, completely different outcomes.

Rob McMillan puts the difference plainly. The wineries that are winning look outward, at their customers, their relationships and their brand. The ones struggling look inward, at cost-cutting, efficiency and operations. As he writes, "you can't cut your way to growth."

The data backs it up. Lower-performing wineries were more than twice as likely to name price cuts and discounting as their main strategy. Successful wineries were 60% more likely to have raised their bottle prices. Discounting still has a role, but as a deliberate tactic inside a value strategy, not as the strategy itself. I see the same instinct here - when things get tight, the first lever a lot of producers reach for is price, and it is rarely the one that works.

DtC is still the engine, but it has stopped growing

Direct-to-consumer still accounts for slightly more than 70% of revenue for the wineries surveyed, with wine club and tasting room doing most of the heavy lifting. That structure has barely changed in a decade.

What has changed is the growth. The channel is no longer expanding. It is stabilising inside a tighter demand environment. The model that drove 30 years of growth is intact, but it is tired, and it was built for a different generation of customer.

This is where I would gently push back on any UK producer who reads it as reassurance. In the US, the smallest producers run DtC shares of 80% and above. In the UK, WineGB's figure for English wine sits at around 30%. I do not read that gap as English wine being behind on quality - it clearly is not. I read it as the infrastructure, the benchmarks and the playbooks for selling direct still being built here. That is headroom, not a verdict.

The digital gap I can't stop thinking about

Here is the finding that stuck with me most, and probably the one I am least objective about. Internet and web sales make up just 6% of the total in the SVB data. The jump in online buying during COVID has quietly unwound, and in some cases digital activity is now below pre-pandemic levels. McMillan's own verdict is blunt: "we can do better there."

For an industry that talks constantly about reaching new and younger customers, that is a remarkable under-investment in the one channel that is not limited by how many people can physically reach the cellar door. The UK wineries I see pulling ahead are the ones treating their website, email list and online store as a genuine sales channel rather than a digital brochure. It is not glamorous work, but the room to move is real and almost nobody is competing for it.

Tasting rooms: cutting the fee is not the fix

Tasting room reservations are in a steady, shallow decline, down roughly 2% to 3% year on year. The instinct for a lot of wineries is to cut the tasting fee. In 2025, 15.5% of them did, double the year before. But only about a quarter saw visitation actually improve.

The lesson is that a lower fee on its own does not bring people in. It works when it is paired with a clear answer to a more basic question: what will make your target customer want to visit in the first place? The higher performers are not racing to the bottom on price. They are increasing spend per guest through curated, one-to-one experiences, which is why average order value is holding up even as footfall softens. I would say exactly the same to any UK producer weighing up whether to drop their tasting price this summer.

Wine clubs: retention is the new growth

The clearest pressure in the whole report is on wine clubs. Net membership growth has fallen from 13% in 2021 to just 2% in 2025. Across the dataset, new sign-ups are roughly cancelled out by people leaving, and the largest clubs are losing members fastest.

And yet the lifetime value of a club member hit a record high of $2,803. The members who stay are worth more than ever. That tells you where the effort belongs. The club has shifted from being a growth engine to being a stabilising force, and retention now matters at least as much as acquisition. Keeping a member engaged between shipments, with reasons to stay that go beyond a discount, is the actual work - and it is the thing I see separating the UK clubs that hold their members from the ones quietly churning them. Rention is often easier and more rewarding than acquisition.

What this means if you sell wine in the UK

Strip the report back and the same handful of jobs apply just as much to a winery in Sussex or Kent as one in Sonoma:

- Compete on perceived value, not on price. Hold your pricing and earn it through experience and brand.

- Treat digital as a real sales channel. Your website, store and email list are the only part of DtC that is not capped by cellar door footfall.

- Make retention a priority, not an afterthought. The members who stay are worth far more than the churn suggests.

- Build relationships beyond the visit, in the places your customers actually live.

None of that is a software problem first. It is a strategy problem. But it is also a large part of why we built Marzipan the way we did - a proper online store, club and subscription management, segmented email and the ability to run and sell events, all in one place - because once a winery decides to do this work, it needs to be possible to actually run without three disconnected tools and a spreadsheet.

Why I want this for the UK

The SVB report is a fixture in the US precisely because it gives wineries somewhere to benchmark themselves, year after year. Here, we have far less to go on.

That bothers me. There is no good UK answer to give a producer who wants to know how they compare, or what the best operators are doing differently. So we are doing something about it. We are running the State of UK Wine Direct-to-Consumer report, to put real numbers behind exactly those questions for English and Welsh producers.

The survey is open now. If you sell wine direct in the UK and want insight like this for our own market, please take a few minutes to take part - everyone who contributes gets the results before they are public. The more producers who take part, the sharper the picture for all of us.